If you’re around 40-years-old and you’ve decided you’re ready to start saving so you can retire at 65, it might be too late.

As we know, the most important factor when it comes to building wealth is time. We also know that the best investment you can make is an investment in an S&P 500 index (like $VOO for example). That index, it’s safe to assume, will return you approximately 10% a year, on average, over the course of approximately 30 years. Hold on to that number: 10%.

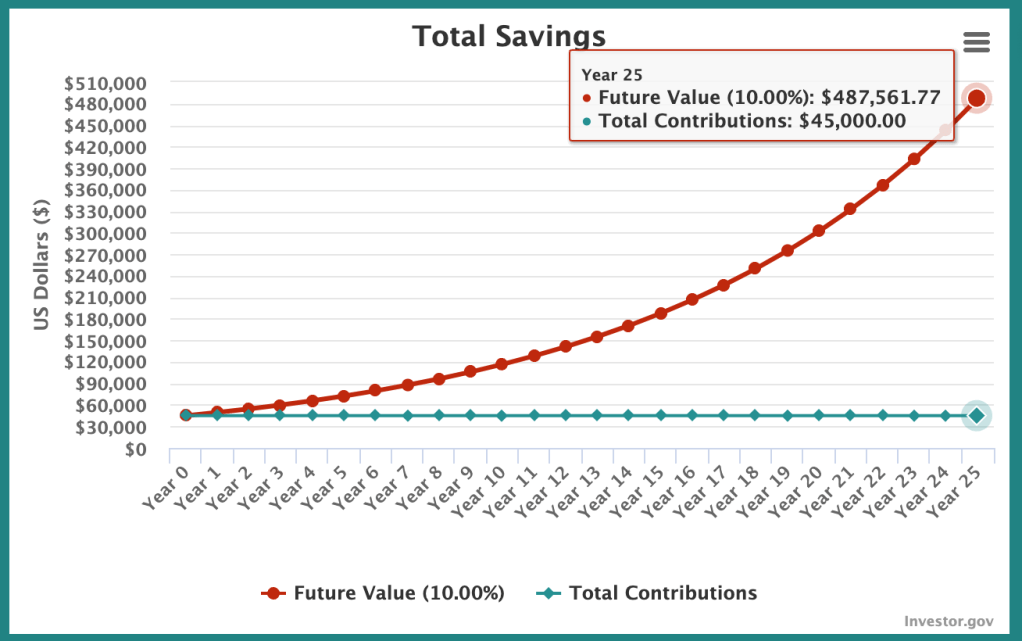

Now, according to the federal reserve, the median amount of money Americans have saved by age 40 is around $45,000. Let’s assume that $45,000 is sitting entirely in $VOO (The S&P 500).

The return on that $45,000 would look like this over 25 years:

After 25 years (or by the time you reach 65 years old), that $45,000 will become $487,562. That’s a great return, but it’s far less than what most people will need to retire.

The chart above also assumes that you will not be making any contributions during that 25 year period which may not be true. From what I can tell, Americans put around $180 towards retirement every month.

Contributing $180/mo to your initial investment of $45,000 for 25 years will give you a return of $699,991. Of course that’s $212,429 more than if you didn’t contribute at all, but it’s still far less than you’ll likely need to retire.

My goal is still to retire someday. What can I do?

If you read the gloomy paragraphs above and said to yourself “I’ll do whatever it takes to retire”, then I highly recommend focusing on your spending.

That’s probably advice you’ve heard before and for good reason. You’re not fully in control of how much you make, but you are in control of how much you spend.

The less you spend, the more you have to invest, the more you have to invest, the more money you have compounding.

You’re right, I’ll never retire. Now what?

Don’t worry, you’re not fated to be miserable everyday just because you’re unable to retire, but what I would recommend, is that you seriously think about what it’ll mean to work until you die.

Do you have a career that’s hard on your body? Better start looking for a career that you can do into old age.

Hate your career? Better start looking for one that you’ll enjoy or can at least tolerate most days of the week because that’s how you’ll be spending most of your remaining time.

Are you a new parent? The good news is that while you may be out of time, your children likely are not. Teach them to save early and set money aside for them as soon as possible.

The math

Unless you’re capable of beating the S&P 500 (and the vast majority of professional investors are not), you should assume that you’ll get an average return of 10% by investing in VOO.

Now it’s just a matter of how much money you can put into VOO and how long you can let it sit there for that’ll determine if you can retire not.

That means your retirement plan is simply this formula: investment(1.1)^years

Investment = the amount of money you can put into VOO

1.1 = the 10% annualized return you’ll get

years = the amount of time you have left.

You can’t control “1.1” or “years“, but you can control “investment“

This article is part of the Winchell House Original Articles series.

You must be logged in to post a comment.